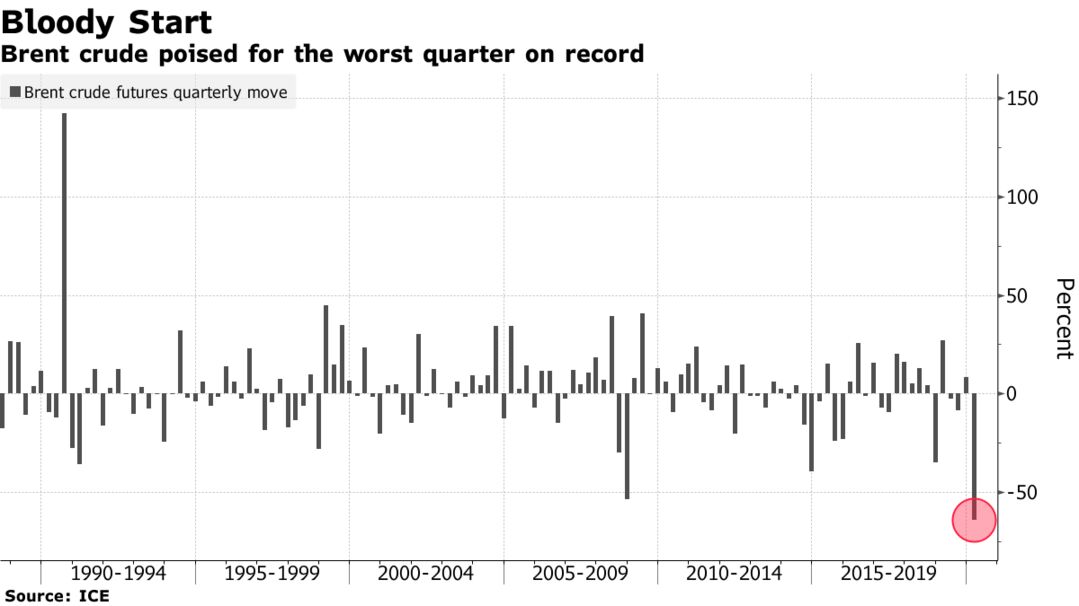

Oil slumped to a 17-year low as coronavirus lockdowns cascaded through the world’s largest economies, leaving the market overwhelmed by cratering demand and a ballooning surplus. Futures in London fell as much as 9.4% to the lowest since November 2002, while New York crude briefly dipped below $20 a barrel. The huge oversupply is further collapsing the oil market’s structure, and there may be more weakness to come as the world quickly runs out of storage capacity.

Prices are on track for the worst quarter on record as demand is hit on an unprecedented scale. Goldman Sachs Group Inc. estimates consumption will drop by 26 million barrels a day this week, while distress signals are spreading with some Indian refiners declaring force majeure on imports. Meanwhile, Riyadh and Moscow are showing no signs of a detente in their supply battle.

“Market participants and oil producers are now shaken to the bone over what is playing out in the oil market,” said Bjarne Schieldrop, chief commodities analyst at SEB AB. “The world cannot store the current surplus.”