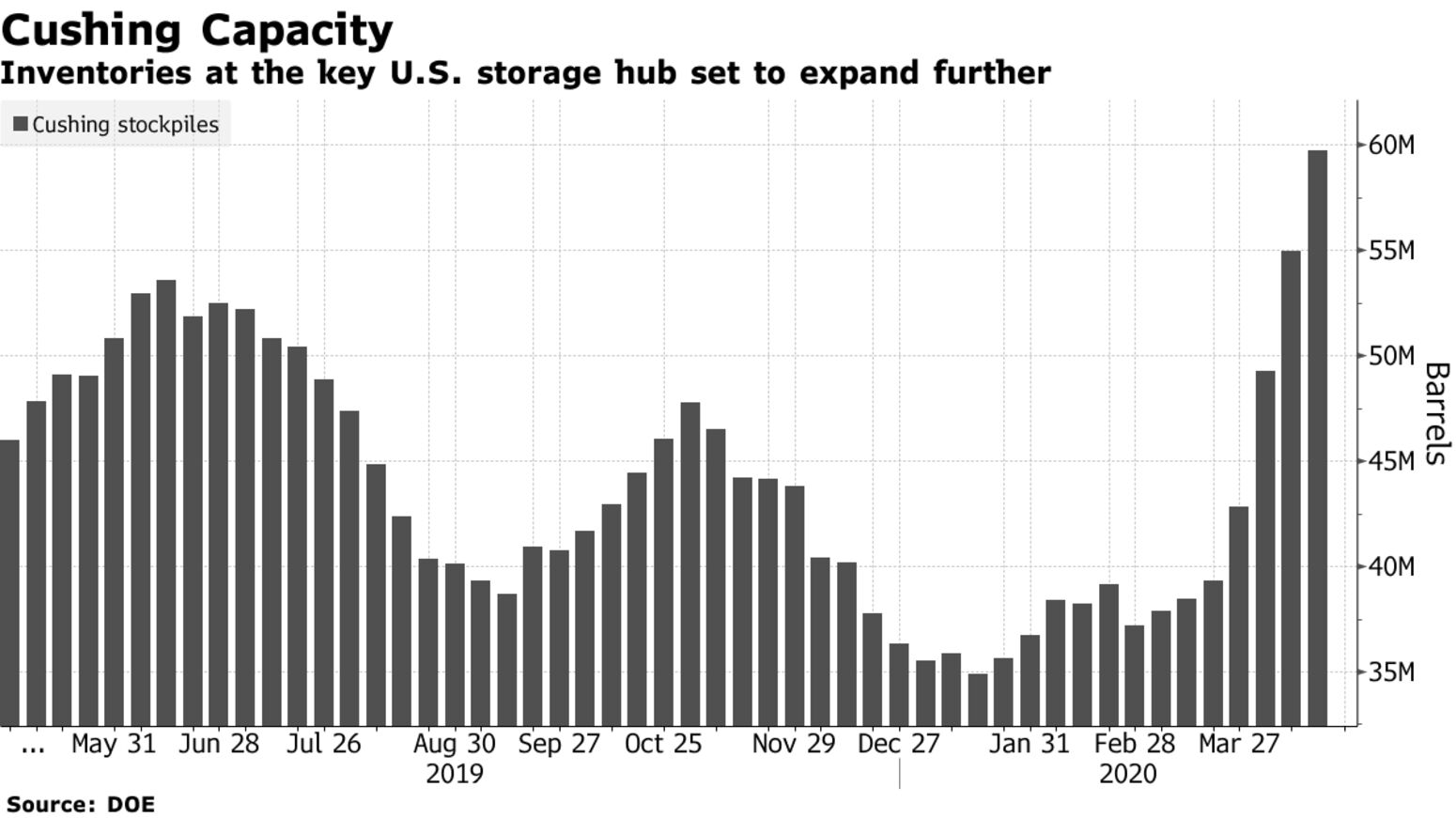

Oil clawed back its recent heavy losses as output cuts from major producers seek to stymie an unprecedented global glut. Futures rose by almost $2 in New York to around $14 a barrel. Russian oil companies will cut output by about 19% from February levels, the nation’s Energy Minister, Alexander Novak told the Interfax news agency. Even at $10 a barrel, some countries are having difficulty selling their oil, highlighting the collapse in demand globally. There have been tentative signs of a recovery in European physical oil markets. Key pricing contracts in the North Sea and Russia have rallied in recent days, though there are still concerns that the world is on the brink of filling its storage capacity. Major producers were due to start output cuts on May 1, but some, including Saudi Arabia, are now curbing output early.

“There is some extra bargain hunting by investors who believe that we may have seen the floor in oil prices,” said Hans Van Cleef, senior energy economist at ABN Amro. “Because of the low base, double-digit price gains or declines seem to be the new normal.” Storage capacity is being tested as a worldwide glut of fuels and crude expands due to the destruction of demand by the coronavirus. Still, there are tentative signs of a fledgling recovery in demand. Spain’s pipeline operator saw more moderate consumption declines than the previous week, while U.S. gasoline sales rose in the week ending April 18, according to OPIS.