Oil rose as the head of the International Energy Agency forecast demand will likely grow past its level before the global pandemic. Futures in New York gained as much as 2.3% on Monday, with trading volumes thin due to holidays in the U.S., U.K. and Singapore. Fatih Birol, executive director of the IEA, said oil consumption hasn’t yet peaked, countering speculation that the virus will have a long-term impact.

“In the absence of strong government policies, a sustained economic recovery and low oil prices are likely to take global oil demand back to where it was, and beyond,” Birol said in an interview, urging governments to focus spending on combating climate change.

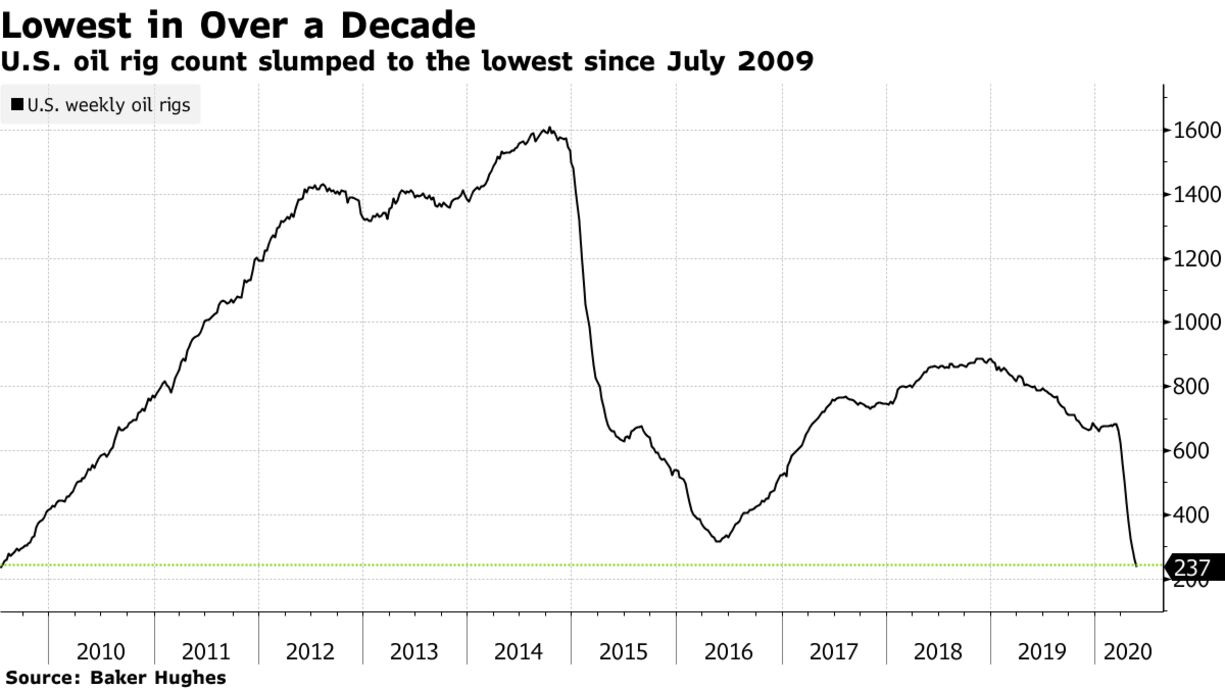

Crude has surged more than 75% this month, following a historic crash in April, as countries began to ease restrictions on people’s movements that were put in place to prevent the spread of the coronavirus. The price recovery has been supported by a faster-than-expected retreat in drilling and production in the U.S. and elsewhere.

“Our view is that the worst is now behind us,” said Daniel Ghali, a TD Securities commodity strategist. “The shale patch is cutting at a phenomenal rate.”

But the return of U.S.-China tensions may limit the scope of oil’s rebound. China warned on Sunday that some in the U.S. were pushing the two countries toward a new Cold War.

The U.S. should give up its “wishful thinking” of changing China, Foreign Minister Wang Yi said during his annual news briefing on the sidelines of National People’s Congress meetings in Beijing. He also warned America not to cross China’s “red line” on Taiwan. “Clearly, we are in an era of heightened geopolitical risk,” Ghali said. “We could see that relationship and the trade between countries get reshuffled.”