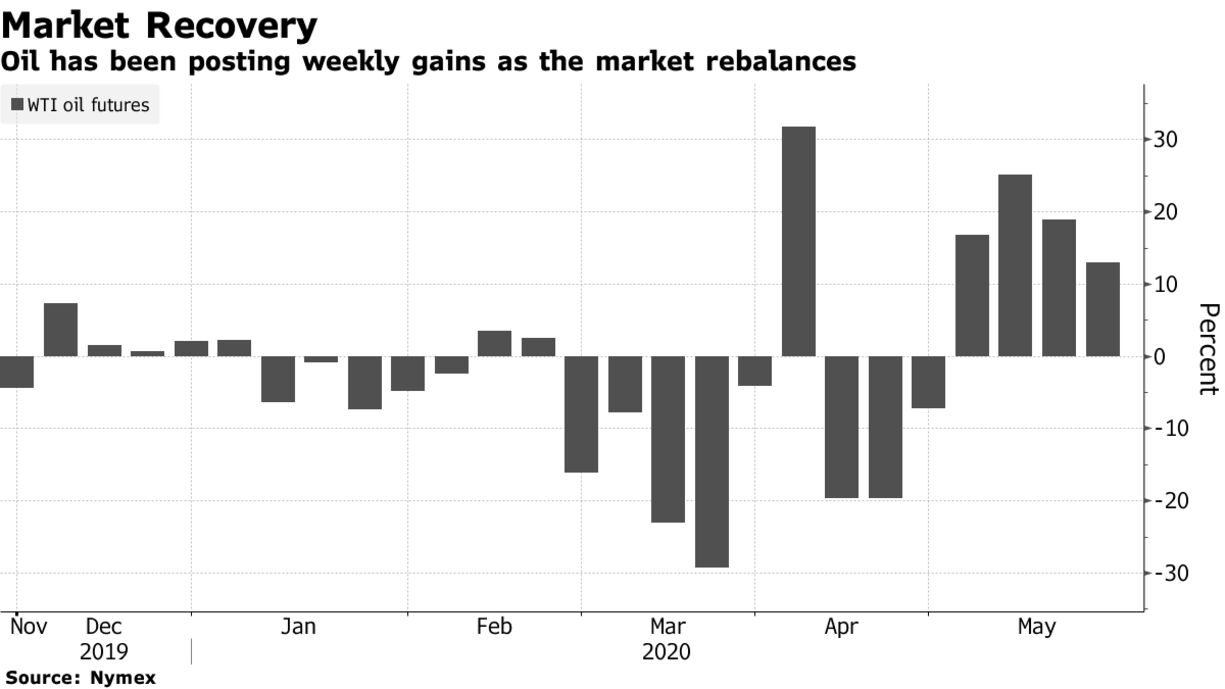

Oil rose above $34 a barrel, following a prediction from Russia that the market may rebalance as early as next month due to historic output cuts from global producers. Russia, a key member of the OPEC+ alliance that has pledged to trim supply by almost 10 million barrels a day, expects the market to balance in June or July. Energy Minister Alexander Novak said global output curbs have so far exceeded those agreed by the coalition. Futures in New York were 2.5% higher from Friday’s close after there was no settlement Monday due to a holiday.

Oil has surged more than 80% this month as demand returned following the easing of lockdown restrictions in some countries, while output cuts have started to chip away at the oversupply. The International Energy Agency sees oil consumption eventually rebounding past pre-virus levels, even as some argue that the coronavirus outbreak will fundamentally shift patterns of consumption.

“Global supply is still heading lower while demand is rising,” said Bjarne Schieldrop, chief commodities analyst at SEB AB. “This all lays the ground for higher prices down the road.”

| PRICES |

|---|

|

Nigeria, which has been stuck with millions of barrels of unsold crude in recent weeks, lifted the selling price for its supplies in June from record lows. Though smaller than in previous months, the discounts remain at unprecedentedly steep levels by historical standards, a reminder of the pockets of oversupply in the market. Around the world, producers have slashed global production by 14 million to 15 million barrels a day so far, Russia’s Novak said on Monday. The nation sees the current global surplus at 7 million to 12 million barrels a day, according to a report from RIA Novosti.