Oil rebounded from a weekly loss as better-than-estimated economic data countered fears that Covid-19’s resurgence will crimp fuel demand. Futures in New York and London closed higher after declining for two out of the last three weeks. Prices followed equities higher as U.S. pending home sales posted a record gain, signaling that America’s economic recovery is underway. Yet the outlook remains uncertain.

“The economic data continues to improve,” said John Kilduff, a partner at Again Capital. The release of China manufacturing data Tuesday, as well as the potential for increased travel during the U.S. July 4 holiday, could turn the next few days into “a make-or-break-it week for oil prices.”

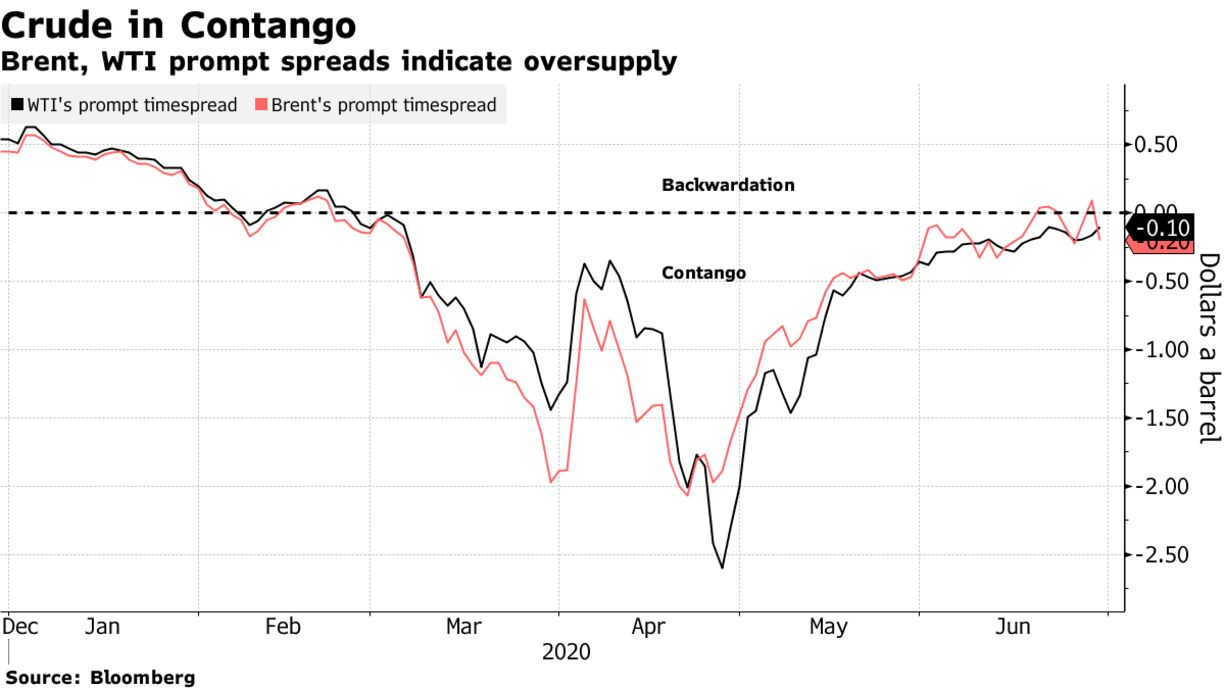

Still, the overall market picture is bearish. Crude stockpiles in the U.S. are at record highs, worldwide consumption remains a long way off pre-virus levels and many refiners are struggling with low margins. In another indication that supplies are plentiful, WTI and Brent crude for prompt delivery are trading at discounts to later dated contacts in a market structure known as contango.

New clusters of coronavirus infections across the U.S. South and Southwest have states including Texas reversing or slowing reopening plans. Domestic fuel consumption dropped 2.3% Saturday from the same day the week prior.

While American gasoline demand has gradually improved, diesel inventories have expanded for 11 out of the last 12 weeks, suggesting that industrial activity has a long road to recovery.

“The product inventory problem may be the most bearish factor out there,” said O’Grady. “If you look at the demand for distillate, it’s terrible, and distillate is what drives the economy,” he said.

| PRICES: |

|---|

|