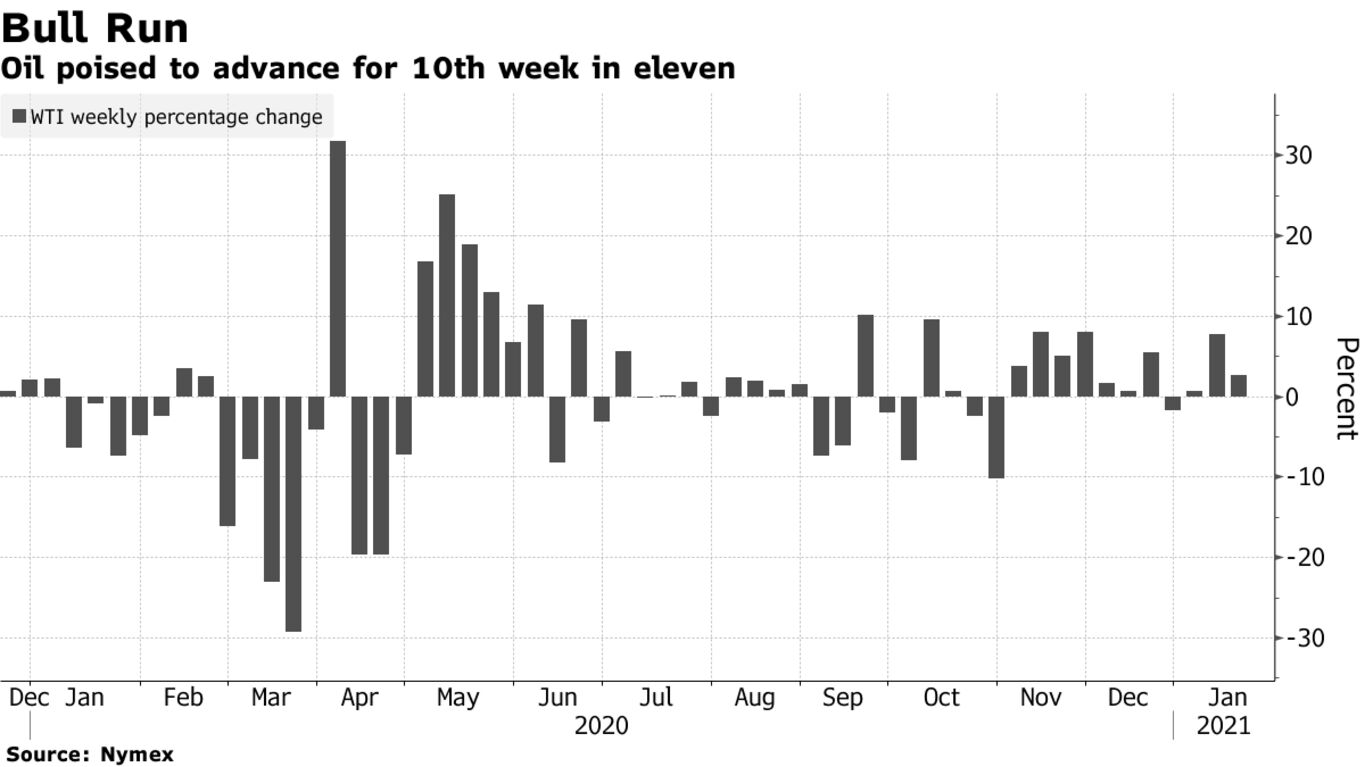

Oil declined from a 10-month high as the dollar strengthened, taking the steam out of a recent rally, while investors assessed what impact a potential U.S. stimulus package will have on driving fuel demand higher. Futures in New York slid 0.9% to trade near $53 a barrel as a stronger dollar reduced the appeal of raw materials like oil that are priced in the currency. President-elect Joe Biden will ask Congress for $1.9 trillion to fund immediate relief for the economy that has been pummeled by the Covid-19 pandemic.

Covid-19 vaccine breakthroughs and a recent pledge by Saudi Arabia to deepen output cuts has driven oil 50% higher since the end of October. Commodities are showing all the signs of a structural bull market, according to Goldman Sachs Group Inc., and OPEC said in its monthly report on Thursday that the group was on track to deplete the world’s bloated crude inventories.

A resurgent virus across some regions, however, may cap further price gains. China is seeing rising cases again after largely containing the outbreak, while in Europe, France is extending tighter curfew measures and Germany is considering strengthening its lockdown.

“I think the market will take a bit of a pause to asses where things sit with so much going on,” said Daniel Hynes, a senior commodity strategist at Australia & New Zealand Banking Group Ltd. in Sydney. “There are plenty of risks at the moment, demand in the shorter term is clearly under pressure.”

| PRICES |

|---|

|